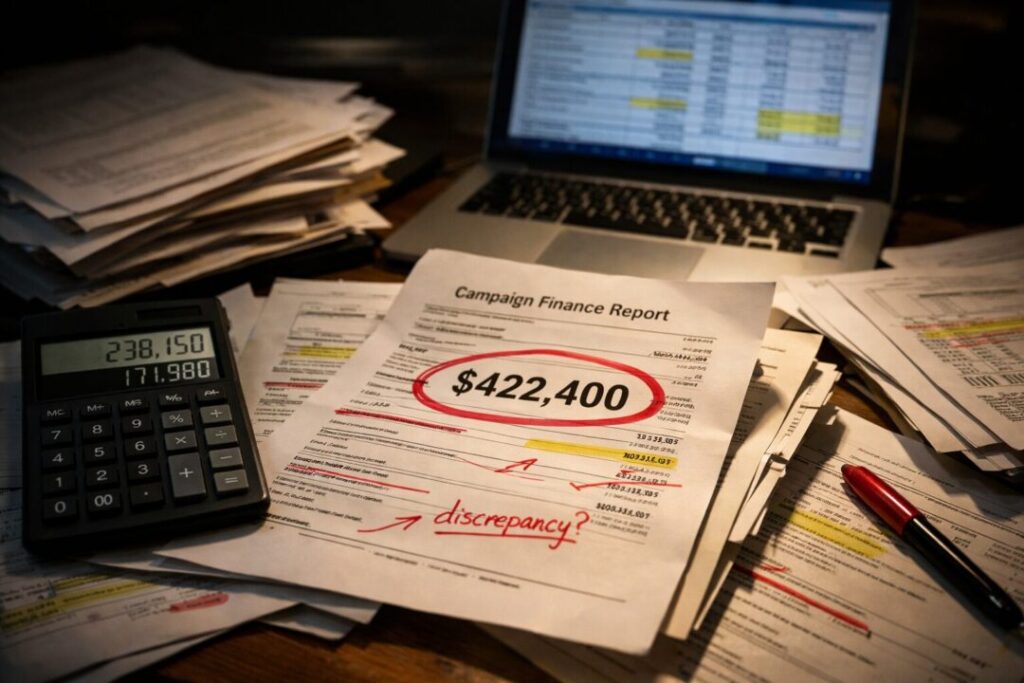

A $422,400 loan. 64 identical transactions. And a paper trail that doesn’t add up.

That’s the heart of a new federal complaint filed against Nevada candidate Drew Johnson, and it’s raising a simple question voters can understand.

Where did the money really come from?

According to the complaint filed April 14, 2026, Johnson and his campaign are accused of possible violations of federal election law tied to that six-figure “personal loan.”

But this wasn’t some normal loan. It didn’t come in one check. It didn’t come in a clean wire transfer.

Instead, the money was broken into 64 separate transactions. Each one for $6,600. The exact legal max an individual can give.

Same number. Over and over. Sixty-four times. That’s not how normal people loan themselves money.

The complaint claims this structure may point to something else entirely. That the money could have come from someone else and been funneled through Johnson’s name.

If that’s true, it’s not a paperwork mistake. It’s illegal. Federal law is crystal clear. You can’t make a contribution in someone else’s name.

Now look at the timing.

The loan hits in mid-August 2024. Thirty-three days later, Johnson lands a spot in the NRCC’s “Young Guns” program.

That’s not just a title. It comes with money, support, and political muscle.

Then just days after that? The campaign pays the entire $422,400 back. In. Out. Gone.

That’s not how struggling campaigns operate. That’s how checkboxes get checked.

And then there’s the part every working Nevadan understands without a law degree: The math.

According to the complaint, Johnson’s own financial disclosures don’t show enough income or assets to cover a loan that big.

After earlier loans, normal living costs, and reported income, the numbers come up short. Way short.

You don’t need to be an accountant to see the problem.

If you make X… And you spend Y… You can’t suddenly produce Z when Z is way bigger than both. Something doesn’t pencil out.

And it doesn’t stop there.

The complaint also claims Johnson failed to disclose a $342,000 mortgage on his home. Not once. Not twice. But on multiple financial filings.

It also points to missing disclosures for crypto sales and dozens of stock trades that should have been reported.

Not optional. Required.

These forms exist for one reason. So voters can see who a candidate is financially tied to. What they own. What they owe. And whether anything doesn’t pass the smell test.

“Drew Johnson’s 2024 campaign finance reports raise legitimate questions about the nature of his so-called ‘personal loans',” said Johnson's GOP primary opponent, Jeff Carter, on the complaint.

“Transparency and compliance with election law is not optional. When transactions are structured in a way that appears inconsistent, it is appropriate to seek answers.”

To be fair, these are allegations. The FEC hasn’t ruled yet. And no one’s been found guilty of anything.

But here’s the real issue: This isn’t about some minor paperwork error. This is about whether the system is being gamed.

Because when a campaign can move nearly half a million dollars in a way that looks like this… when the numbers don’t line up… when required disclosures are missing…

That’s not a typo. That’s a red flag.

And voters aren’t stupid. They know the difference between a mistake… and something that was done on purpose.

In a state like Nevada, where elections are often decided by a handful of votes, this matters. A lot.

Because if a candidate can’t give straight answers about their own money, why should anyone trust them with yours?

The opinions expressed by contributors are their own and do not necessarily represent the views of Nevada News & Views. Digital technology was used in the research, writing, and production of this article. Please verify information and consult additional sources as needed.